EIA Short-Term Energy Outlook

Release Date: Sept. 9, 2015

Highlights

- North Sea Brent crude oil prices averaged $47/barrel (b) in August, a $10/b decrease from July. This third consecutive monthly decrease in prices likely reflects concerns about lower economic growth in emerging markets, expectations of higher oil exports from Iran, and continuing growth in global inventories. Crude oil price volatility increased significantly, with Brent prices showing daily changes of more than 5% for four consecutive trading days from August 27 to September 1, the longest such stretch since December 2008.

- EIA forecasts that Brent crude oil prices will average $54/b in 2015 and $59/b in 2016, unchanged from last month’s STEO. Forecast West Texas Intermediate (WTI) crude oil prices in 2015 and 2016 average $5/b lower than the Brent price. The current values of futures and options contracts for December 2015 delivery (Market Prices and Uncertainty Report) suggest the market expects WTI prices to range from $32/b to $73/b (at the 95% confidence interval) in December 2015.

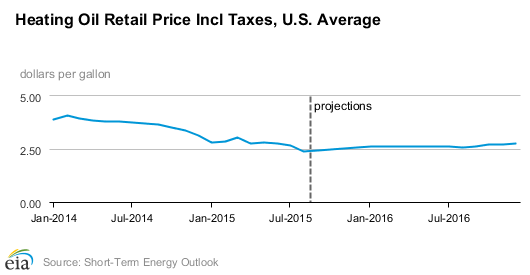

- S. regular gasoline monthly retail prices averaged $2.64/gallon (gal) in August, a decrease of 16 cents/gal from July and 85 cents/gal lower than in August 2014. EIA expects monthly gasoline prices to decline from the August level to an average of $2.11/gal during the fourth quarter of 2015. EIA forecasts U.S. regular gasoline retail prices to average $2.38/gal in 2016.

- EIA estimates total U.S. crude oil production declined by 140,000 barrels per day (b/d) in August compared with July production. Crude oil production is forecast to continue decreasing through mid-2016 before growth resumes late in 2016. Projected U.S. crude oil production averages 9.2 million b/d in 2015 and 8.8 million b/d in 2016, which are both 0.1 million b/d lower than in the prior STEO.

- Natural gas working inventories were 3,193 billion cubic feet (Bcf) on August 28. This level was 18% higher than a year ago and 4% higher than the previous five-year average (2010-14) for this week. EIA projects inventories will close the injection season at the end of October at 3,840 Bcf, which would be the third-highest end-of-October level on record.