EIA: As U.S. Propane Production and Export Capacity Expand, U.S. Propane Exports Reach More Distant Markets

Excerpted from This Week in Petroleum- Oct. 28, 2015

The combination of significant U.S. propane production increases over the past seven years and relatively slow domestic demand growth has reversed historical trade positions. The United States has gone from being a net propane importer to a net exporter, facilitated by rapid expansion in export capacity of domestic supply. Propane exports from the United States are changing traditional propane market patterns across the globe.

The initial growth in U.S. propane production, between 2008 and 2010, caused a reduction in dependence on propane imports, with net imports falling from an average of 109,000 barrels per day (b/d) in 2008 to a near-balance of 16,000 b/d in net exports in 2010. By 2011, only Canada remained as a major supplier of imported propane into the United States, with overseas imports relegated to occasional seasonal shipments into the Northeast and delivery to Hawaii. As propane production and export capacity continued to grow, so did the reach of U.S. propane exports.

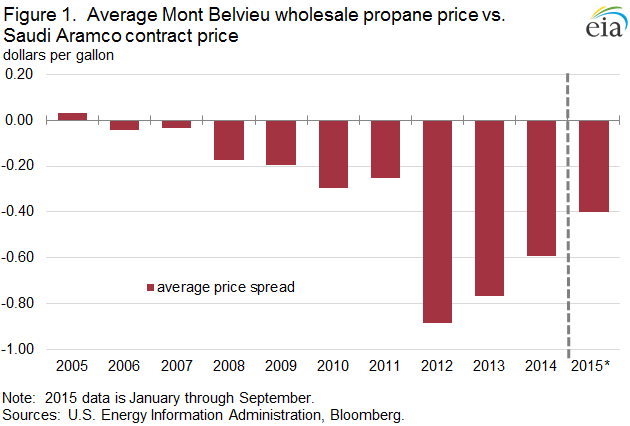

Demand for U.S. propane exports is driven by favorable pricing for U.S. propane compared with the international market, where prices are typically set by the Saudi Aramco monthly contract price (ACP). Saudi Aramco generally bases its propane price on naphtha, a light petroleum product created through the processing of crude oil in a refinery and the competing petrochemical feedstock to propane. In 2005, when the United States was still a net importer of propane, the U.S. price of propane at Mont Belvieu, Texas, averaged a 3-cent per gallon (gal) premium to ACP (Figure 1). As growing U.S. propane exports reached terminal capacity limits, Mont Belvieu prices became discounted compared with the international market, averaging an 89-cent/gal discount in 2012. The wide price differential prompted new export capacity terminal construction, providing an outlet for stranded U.S. propane into the international market. With the expansion of export capacity in the United States, the spread between international and U.S. propane prices has gradually narrowed. The discount for Mont Belvieu propane prices compared with ACP declined from an average of 77 cents/gal in 2013 and 59 cents/gal in 2014 to 40 cents/gal for January through September 2015.

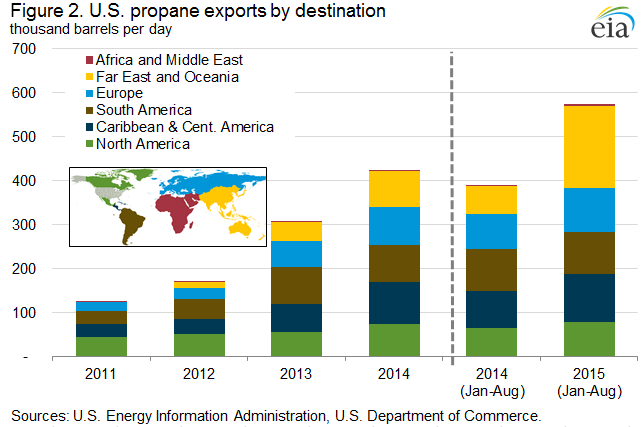

U.S. exports of propane were initially sent to nearby markets in Mexico, the Caribbean, and South America. U.S. exports to these destinations more than doubled between 2010 and 2013, from 88,000 b/d to 198,000 b/d (Figure 2). Previously, these regions had relied on supply from Trinidad and Tobago, Venezuela, and more distant sources, including European, African, and Middle Eastern producers. U.S. propane exports to the region have saturated the Central American and South American markets, displacing most imports from outside the Western Hemisphere. Consumer heating and cooking account for most of the propane demand in South America, which has a counterseasonal propane demand profile compared with the United States. Though no major propane-fed petrochemical projects have been announced in this region, several propane-fueled power generation projects are being planned, which could draw on U.S.-sourced propane.

By the latter half of 2013, substantial quantities of U.S. propane exports were being sent to the European market, helping to offset declines in regional propane production. The traditional markets for propane in Europe are the off-grid consumer space heating and cooking market, which peaks in the winter, and the petrochemical sector, where demand is greatest in the summer. Between 2012 and 2013, U.S. propane exports to Europe more than doubled, from 25,000 b/d to 59,000 b/d. Thus far in 2015, average exports to Europe are running at nearly 100,000 b/d. U.S. propane exports are now competing with Europe’s traditional import sources, particularly Russia, North Africa, and the Middle East.

The Asian propane market is expected to be the leading source of global propane consumption growth. U.S. propane exports to Asia nearly tripled in 2015, from 65,000 b/d in the first eight months of 2014 to 189,000 b/d in the same months of 2015. Asia is the destination for most of the incremental growth in U.S. exports, which can be seen by comparing the first eight months of 2014 to 2015 (Figure 2). Traditionally, Asia is supplied by imports from the Middle East and by in-region refinery and gas plant production. Uses of propane in Asia vary significantly across the region. The traditional consumer space heating and cooking fuel demand sector represents most of the demand in India and Indonesia, plays a prominent role in China, and is expected to grow as consumers shift from dung, wood, and kerosene to propane. Across Asia, propane (or LPG-a propane/butane blend) is also a major transportation fuel, with South Korea and Thailand among the top five markets in the world for LPG-fueled vehicles. In Japan, most propane is consumed in off-grid residential applications, and propane is also blended into imported liquefied natural gas (LNG) to boost the heat value of natural gas to meet Japanese pipeline quality specifications.

Throughout most of 2013 and 2014, propane was one of the most attractive feedstocks for petrochemical crackers. Growth in U.S. propane exports is likely to be driven by global petrochemical demand. Incremental growth in European consumption is expected to come primarily from the petrochemical sector, including potential new propane dehydrogenation (PDH) plants. In Asia, the fastest-growing segment of propane demand is the petrochemical sector, with significant growth in PDH capacity. Since 2013 China began to build out its PDH capacity and currently has seven operational PDH plants. At nameplate capacity, these plants consume an estimated 200,000 b/d of propane feedstock, in addition to the estimated 50,000 b/d of propane demand by PDH units in other Asian countries. If current pricing trends continue, growing petrochemical demand, especially in Asia, will be the primary market for further increases in U.S. propane exports.